As the U.S. stock market shows signs of strength, with the S&P 500 recently hitting a record high, investors are closely monitoring economic indicators and Federal Reserve policies that could influence market dynamics. In this environment, identifying undervalued small-cap stocks with potential for growth becomes particularly compelling, especially when insider actions suggest confidence in these companies’ prospects.

Top 10 Undervalued Small Caps With Insider Buying In The United States

|

Name |

PE |

PS |

Discount to Fair Value |

Value Rating |

|---|---|---|---|---|

|

Hanover Bancorp |

8.7x |

2.0x |

47.42% |

★★★★★☆ |

|

AtriCure |

NA |

2.8x |

47.12% |

★★★★★☆ |

|

Titan Machinery |

4.0x |

0.1x |

23.49% |

★★★★★☆ |

|

Columbus McKinnon |

22.1x |

1.0x |

46.43% |

★★★★☆☆ |

|

Franklin Financial Services |

8.9x |

1.8x |

37.10% |

★★★★☆☆ |

|

Citizens & Northern |

13.0x |

2.9x |

37.52% |

★★★☆☆☆ |

|

Ramaco Resources |

14.4x |

1.2x |

9.15% |

★★★☆☆☆ |

|

Community West Bancshares |

18.7x |

2.9x |

42.25% |

★★★☆☆☆ |

|

Delek US Holdings |

NA |

0.1x |

-134.74% |

★★★☆☆☆ |

|

Alta Equipment Group |

NA |

0.2x |

-199.30% |

★★★☆☆☆ |

Here’s a peek at a few of the choices from the screener.

Simply Wall St Value Rating: ★★★★★☆

Overview: Advantage Solutions is a business solutions provider specializing in sales and marketing services with a market capitalization of approximately $2.43 billion.

Operations: From 2014 to 2024, the company experienced fluctuations in its gross profit margin, which ranged from a high of approximately 23.28% in earlier years to a low of around 13.36% by the end of the period. Notably, revenue grew from $1.71 billion in 2014 to over $4.15 billion by mid-2024, indicating significant expansion despite varying profitability metrics during this decade.

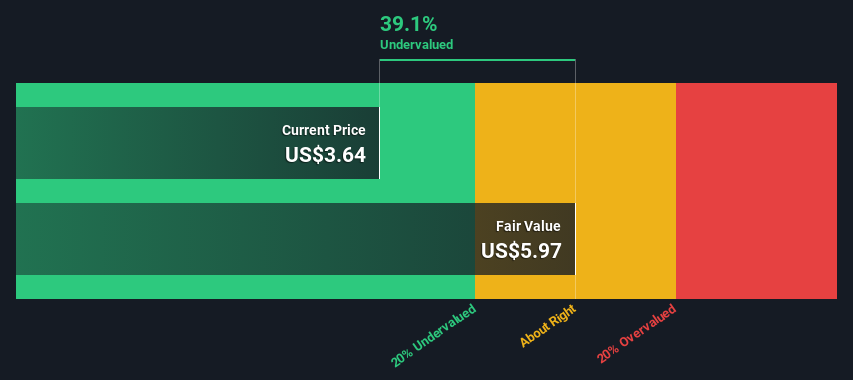

PE: -15.7x

Despite being recently dropped from several Russell indexes, Advantage Solutions shows promise through strategic initiatives like the upcoming joint venture with L.A. Libations, aimed at expanding their reach in the consumer packaged goods sector. This move could enhance their market presence significantly, leveraging both companies’ strengths. Financially, they’ve shown confidence with a recent buyback of 5 million shares for US$20 million, signaling insider confidence in their growth trajectory. Additionally, after a challenging period with a net loss reduction from US$47.59 million to US$5.31 million year-over-year as of Q1 2024, these actions suggest potential for recovery and growth despite current unprofitability forecasts.

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Hertz Global Holdings operates a vehicle rental business primarily through its segments in the Americas and internationally, with a market capitalization of approximately $4.30 billion.

Operations: The company generates revenue of $9.40 billion, with a notable gross profit margin increase to 12.56% in the latest quarter from previous periods. It incurs significant costs of goods sold (COGS), totaling $8.22 billion, impacting its overall profitability.

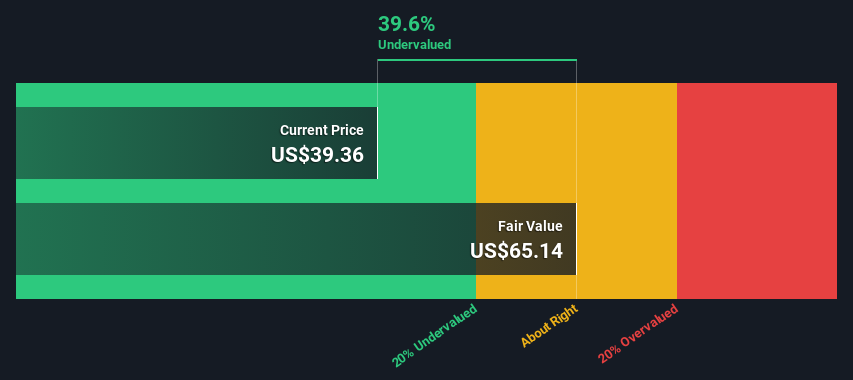

PE: 5.6x

Amidst a backdrop of strategic leadership enhancements and index reclassifications, Hertz Global Holdings exemplifies a promising yet undervalued entity within the small-cap landscape. Recently appointed executives aim to refine operations and boost profitability, signaling a robust commitment to operational excellence. Insider confidence is evident as they recently purchased shares, underscoring belief in the company’s direction. With its addition to the Russell 2000 Index on July 1, 2024, Hertz is positioned for potential growth amidst financial recalibrations and market realignments.

Simply Wall St Value Rating: ★★★★★☆

Overview: Shutterstock operates as a global provider of stock photography, stock footage, stock music, and editing tools with a market cap of approximately $2.87 billion.

Operations: The company generates revenue by providing internet information services, with a recent quarterly revenue reported at $873.62 million. It has seen a net income of $93.55 million for the same period, reflecting a net income margin of approximately 10.71%.

PE: 15.5x

Shutterstock’s recent appointment of Jaime Teevan to its board underscores a strategic push into AI and machine learning, enhancing its data offerings—a move aligning with its forecasted 18.53% annual earnings growth. Insider confidence is evidenced by their recent share purchases, signaling belief in the company’s direction. Additionally, inclusion in several Russell indexes suggests recognition of its potential in the market. With revenue guidance up to US$936 million for 2024, Shutterstock is poised for significant growth amidst expanding enterprise demand.

Where To Now?

Ready To Venture Into Other Investment Styles?

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include NasdaqGS:ADV NasdaqGS:HTZ and NYSE:SSTK.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com