Amidst a fluctuating U.S. market landscape, where recent inflation data has sparked optimism for potential interest rate cuts by the Federal Reserve, investors are closely monitoring opportunities across various sectors. In such a context, identifying undervalued small-cap stocks like Univest Financial becomes particularly compelling as these entities may benefit significantly from broader economic shifts and market sentiment adjustments.

Top 10 Undervalued Small Caps With Insider Buying In The United States

|

Name |

PE |

PS |

Discount to Fair Value |

Value Rating |

|---|---|---|---|---|

|

Hanover Bancorp |

8.5x |

1.9x |

47.08% |

★★★★★☆ |

|

Thryv Holdings |

NA |

0.8x |

24.30% |

★★★★★☆ |

|

Papa John’s International |

18.1x |

0.6x |

40.68% |

★★★★☆☆ |

|

Franklin Financial Services |

9.9x |

2.0x |

30.45% |

★★★★☆☆ |

|

Columbus McKinnon |

24.4x |

1.1x |

42.67% |

★★★★☆☆ |

|

Titan Machinery |

4.3x |

0.1x |

17.65% |

★★★★☆☆ |

|

Chatham Lodging Trust |

NA |

1.4x |

13.08% |

★★★★☆☆ |

|

Citizens & Northern |

14.4x |

3.2x |

31.43% |

★★★☆☆☆ |

|

Community West Bancshares |

18.7x |

2.9x |

42.25% |

★★★☆☆☆ |

|

Delek US Holdings |

NA |

0.1x |

-142.93% |

★★★☆☆☆ |

Let’s dive into some prime choices out of from the screener.

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Univest Financial is a financial services provider offering banking, insurance, and investment solutions with a market capitalization of approximately $0.75 billion.

Operations: The company generates revenue through its operations, consistently achieving a gross profit margin of 100% across multiple reporting periods. Notably, the net income margin has shown variation, reaching as high as approximately 35% in recent quarters.

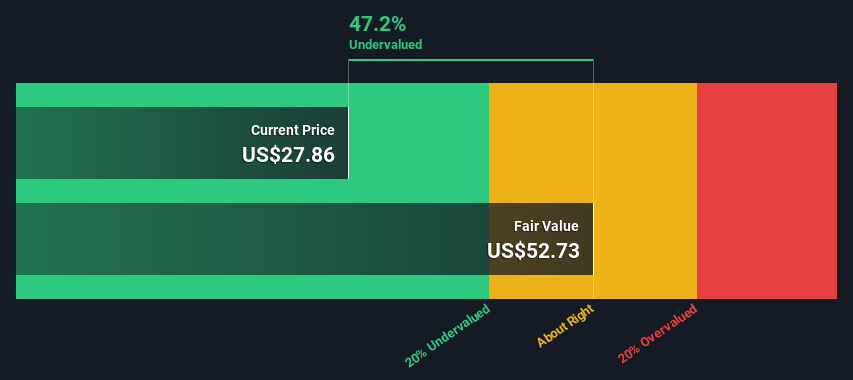

PE: 11.9x

Despite a slight dip in net interest income, Univest Financial reported an increase in net income to US$18.11 million for Q2 2024, up from US$16.8 million in the previous year, showcasing resilience and potential undercurrents of growth. With earnings per share also rising, this reflects positively on operational efficiency. Recently, insider confidence was bolstered as evidenced by share purchases made by insiders during this period of financial reporting. Additionally, their recent presentation at the KBW Community Bank Investor Conference could signal strategic positioning for future prospects despite forecasts suggesting a potential average earnings decline over the next three years.

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Delek US Holdings is an energy company primarily engaged in petroleum refining, with additional operations in logistics and retail, boasting a market capitalization of approximately $1.07 billion.

Operations: Refining constitutes the major revenue stream for this entity, generating $15.72 billion, complemented by contributions from retail and logistics segments amounting to $871.2 million and $1.03 billion respectively. The gross profit margin observed a notable increase from 10.27% to 6.12% over the analyzed periods, reflecting changes in cost of goods sold and revenue dynamics without maintaining a consistent trend year-over-year.

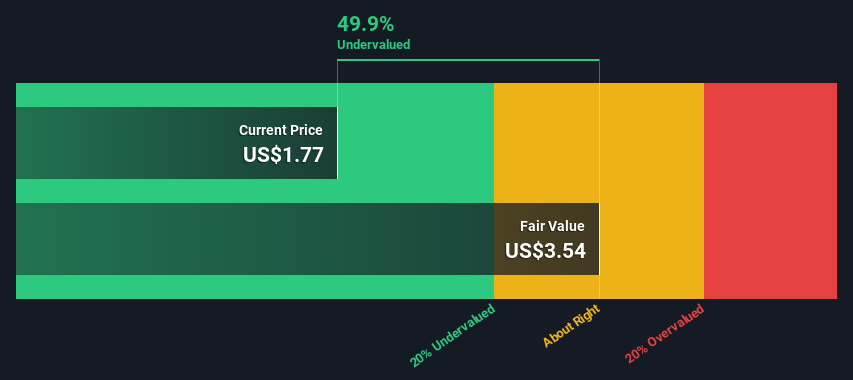

PE: -19.9x

Recently added to multiple Russell indexes, Delek US Holdings signifies a promising yet underappreciated asset within the small-cap spectrum. Despite a challenging first quarter in 2024, where sales dipped and losses were reported, their strategic adjustments include an increased quarterly dividend and significant share repurchases completed by March 2024—highlighting strong internal confidence and commitment to shareholder value. This blend of financial resilience and insider confidence, with no recent insider purchases to report, positions them intriguingly for astute investors looking at overlooked market segments.

Simply Wall St Value Rating: ★★★★★☆

Overview: Lumen Technologies is a telecommunications company that operates in various segments, including business and mass markets, with a market capitalization of approximately $10.34 billion.

Operations: The company’s gross profit margin has shown a downward trend over the past decade, decreasing from approximately 61.25% in late 2013 to about 50.54% by mid-2024, reflecting increasing costs of goods sold relative to revenue. Notably, its net income has fluctuated significantly during this period, with substantial losses recorded from early 2023 onwards.

PE: -0.2x

Lumen Technologies, a firm often overlooked, recently showcased its robust strategic moves, including a promising partnership with Microsoft aimed at enhancing digital infrastructure—a key growth vector. This collaboration is poised to bolster Lumen’s cash flow significantly by over US$20 million in the upcoming year. Additionally, insider confidence was evident as they recently purchased shares, signaling belief in the company’s trajectory. With these developments, Lumen positions itself as an intriguing entity within the undervalued sector.

Where To Now?

Seeking Other Investments?

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include NasdaqGS:UVSP NYSE:DK and NYSE:LUMN.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com