The past three years have been fantastic for Micron Technology (MU 0.77%) investors, as a $1,000 investment made in its shares three years ago is now worth an impressive $7,100. What’s worth noting is that a significant chunk of these gains has arrived in the past year, once it became evident that Micron is playing a critical role in the global artificial intelligence (AI) infrastructure build-out.

Micron stock has benefited from the supply-constrained memory market. AI-fueled memory demand has significantly outpaced the available supply, resulting in a sharp spike in memory prices. The favorable pricing environment has been a boon for Micron’s revenue and earnings, and the market has rewarded the stock handsomely for its terrific growth.

But will this catalyst last for the next three years and help Micron deliver more gains?

Image source: Micron Technology.

The memory supercycle is expected to last until 2028

Memory demand isn’t going to slow down anytime soon, driven primarily by the booming demand for data center-specific memory chips known as high-bandwidth memory (HBM). HBM consumption is increasing at a breathtaking pace. That isn’t surprising, as HBM plays a pivotal role in moving large amounts of data at high speeds in AI data centers, while consuming less energy than traditional dynamic random-access memory (DRAM) chips.

This explains why Micron is bullish about the growth of the global HBM market, pointing out in its December 2024 earnings call: “The HBM market will exhibit robust growth over the next few years. In 2028, we expect the HBM total addressable market (TAM) to grow 4 times from the $16 billion level in 2024 and to exceed $100 billion by 2030.”

Today’s Change

(-0.77%) $-3.19

Current Price

$412.37

Key Data Points

Market Cap

$464B

Day’s Range

$401.18 – $417.96

52wk Range

$61.54 – $455.50

Volume

29M

Avg Vol

32M

Gross Margin

45.53%

Dividend Yield

0.11%

What’s worth noting is that Micron pointed out in its December 2025 earnings call that it expects the HBM market’s revenue to hit $100 billion in 2028, two years earlier than expected. The aggressive investment in AI data centers explains this upgraded forecast. Nvidia, for instance, is anticipating data center capital expenditures (capex) to increase at a 40% annual rate through 2030. As HBM plays an important role in AI data center chips, it should remain in strong demand over this period as well.

So, it is easy to see why key memory industry players like Micron and SK Hynix are forecasting the shortage to last until 2028. This should pave the way for further price increases, which is precisely why Micron’s impressive rally could continue for the next three years.

Here’s how much upside investors can expect from the stock

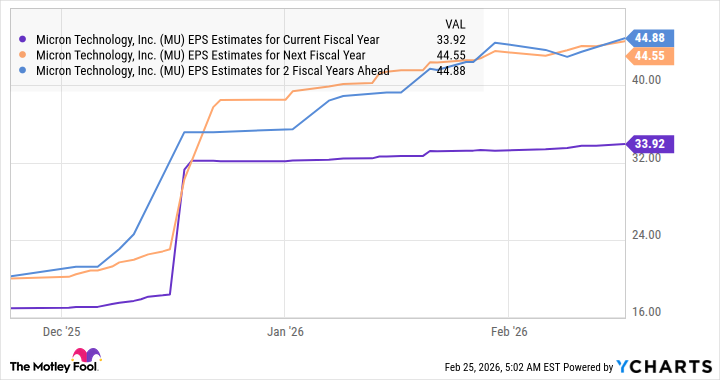

Micron finished its fiscal 2025 (which ended on Aug. 28, 2025) with $8.29 per share in adjusted earnings. The following chart makes it clear that its bottom-line growth is poised to take off.

MU EPS Estimates for Current Fiscal Year data by YCharts

Analysts aren’t expecting a major jump in Micron’s earnings in fiscal 2028 as compared to fiscal 2027 levels. But the persistent supply shortage in the memory industry, as discussed above, indicates that it could clock another year of terrific earnings growth in fiscal 2028.

Even if we assume Micron’s earnings hit $44.88 per share after three years and it trades at 25 times forward earnings at that time (in line with the Nasdaq-100 index and using the index as a proxy for tech stocks), its stock could hit $1,135. That would be a potential jump of 171% from current levels, which means that this AI stock remains worth buying even now.