Chris Jennings is a writer and editor with more than seven years of experience in the personal finance and mortgage space. He enjoys simplifying complex mortgage topics for first-time homebuyers and homeowners alike. His work has been featured in a number of outlets, including Yahoo Finance, MSN, Fox Business, and GOBankingRates.

Chris Jennings is a writer and editor with more than seven years of experience in the personal finance and mortgage space. He enjoys simplifying complex mortgage topics for first-time homebuyers and homeowners alike. His work has been featured in a number of outlets, including Yahoo Finance, MSN, Fox Business, and GOBankingRates.

Editorial Note: We earn a commission from partner links on Forbes Advisor. Commissions do not affect our editors’ opinions or evaluations.

Here are the average annual percentage rates (APR) today on 30-year, 15-year and 5/1 ARM mortgages:

What Are Today’s Mortgage Rates?

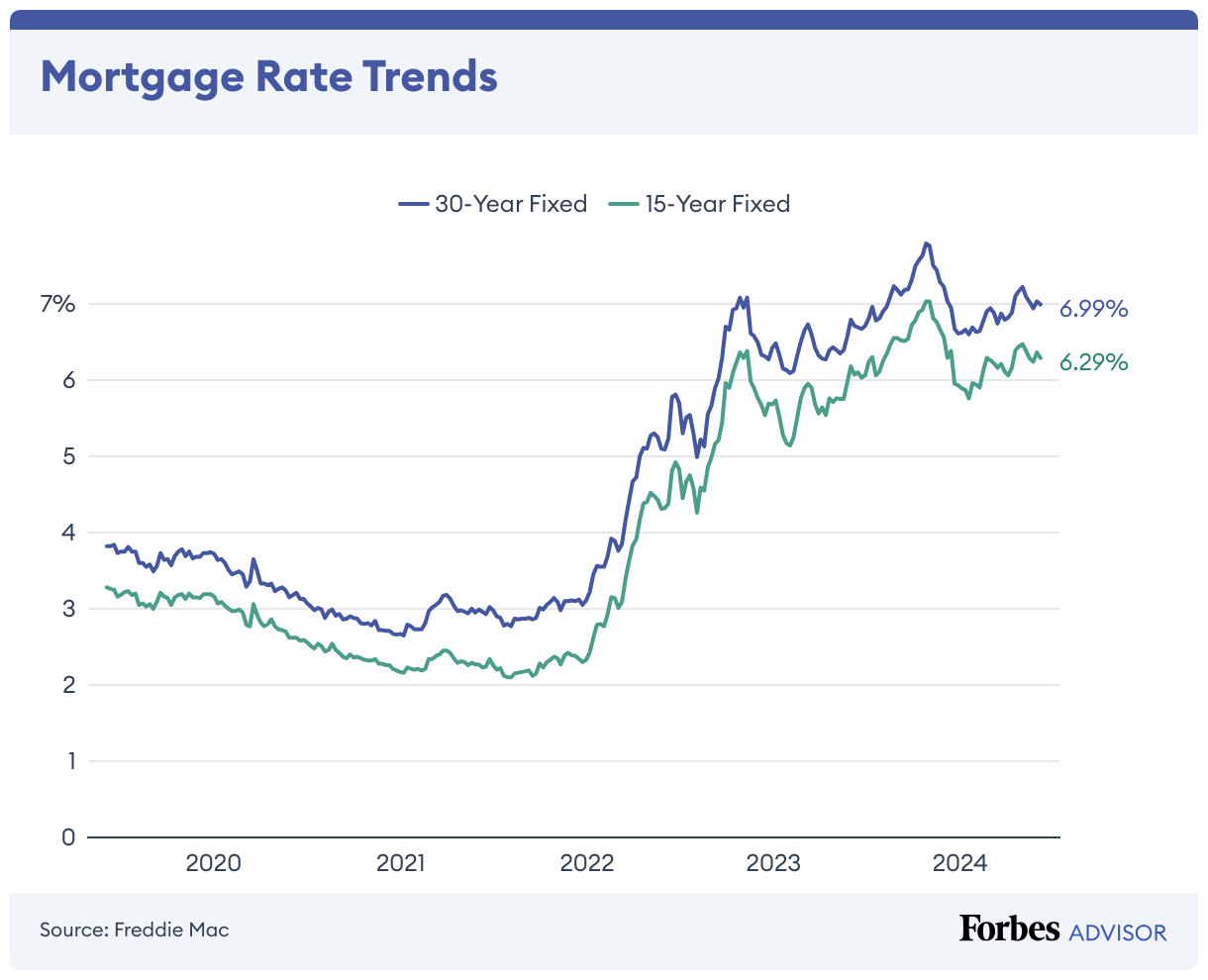

30-year fixed-rate mortgage:

- Today. The average APR for the benchmark 30-year fixed mortgage is 7.42%

- Last week. 7.39%

15-year fixed-rate mortgage:

- Today. The average APR on a 15-year fixed-rate mortgage is 6.74%

- Last week. 6.66%

30-year fixed-rate jumbo mortgage:

- Today. The average APR on the 30-year fixed-rate jumbo mortgage is 7.40%

- Last week. 7.40%

Mortgage Rate Trends

Read In-Depth Mortgage Rates Analysis by Day

Today’s Mortgage Interest Rates by Term

*Source: Curinos

Forbes Advisor Average Mortgage Rates for June 2024

While rates remain elevated, the Fed recently signaled that it will begin to cut rates in 2024, indicating a further downward shift in mortgage rates may soon come.

Regardless of which direction mortgage rates head, you’ll want to compare rates and terms among the best mortgage lenders to find a deal that fits your unique situation.

Insights From Economists: Detailed Predictions for Interest Rates in June 2024

- Bright MLS chief economist Dr. Lisa Sturtevant. “The Federal Reserve has indicated that there will likely be cuts to the short-term federal funds rate in 2024, which will put downward pressure on mortgage rates. Overall, though, rates are expected to remain above 6% throughout [2024].”

- William Raveis Mortgage regional vice president Melissa Cohn. “The peak in mortgage rates is behind us, but mortgage rates are not going to decline as fast as everyone would like them to. … The Fed and the markets will now closely analyze all data, and when there is a consistent flow of weaker data, the door will be opened for the Fed to initiate their first rate cut, hopefully, at the end of the second quarter.”

- First American deputy chief economist Odeta Kushi. “The ongoing deceleration in inflation, coupled with the Federal Reserve’s recent indication of potential rate cuts [in 2024], suggests an environment supportive of modest declines in mortgage rates. Barring any unforeseen circumstances and resurgence in inflation, lower mortgage rates could be on the horizon, but the journey towards them might be slow and bumpy.”

- Hometap Equity Partners head of investor product Dan Burnett. “While softening economic data and indications from the Fed hint that the rate cut cycle could begin sooner than expected, it is worth proceeding with caution as it pertains to mortgage rates. Fed policy will be contingent on continued progress on inflation. If current trends continue, consumers can expect to see Treasury yields decline and mortgage rates come down along with them.”

- Zillow chief economist Skylar Olsen. “I’m expecting mortgage rates to be a bit less volatile in 2024 and, data surprises aside, continue to slowly ease down over the course of the year.”

Check your rates today with Better Mortgage.

Faster, easier mortgage lending

How Today’s Interest Rates Affect Your Monthly Payments

If you know how much you’re borrowing, what type of loan you’re getting and how many years you have to pay it back, you can use a mortgage calculator to check your monthly payment at different interest rates.

For instance, if you have a starting loan balance of $425,000 on a 30-year fixed-rate mortgage, here’s approximately what you can expect to pay in principal and interest every month, excluding taxes, mortgage insurance, homeowners insurance and HOA fees:

- At a 5% interest rate. $2,281 in monthly payments (excluding taxes, mortgage insurance, homeowners insurance and HOA fees)

- At a 6% interest rate. $2,548 in monthly payments (excluding taxes, mortgage insurance, homeowners insurance and HOA fees)

- At a 7% interest rate. $2,828 in monthly payments (excluding taxes, mortgage insurance, homeowners insurance and HOA fees)

- At an 8% interest rate. $3,119 in monthly payments (excluding taxes, mortgage insurance, homeowners insurance and HOA fees)

How To Get the Best Mortgage Rate Today

Though lenders decide your mortgage rate, there are some proactive steps you can take to ensure the best rate possible. For example, advanced preparation and meeting with multiple lenders can go a long way. Even lowering your rate by a few basis points can save you money in the long run.

Here are some other ways you can improve your chances of getting the best deal:

- Take stock of your financial situation. Before you fall in love with your dream home, you better make sure you can afford the monthly payments and other homeownership costs. For instance, start by looking at your debt-to-income (DTI) ratio—aka your total monthly debts against your monthly earnings—to determine how much home you can afford.

- Review your credit score. Lenders look at your credit score to evaluate the risk you pose as a borrower. A higher score gives you a better chance at scoring favorable mortgage terms. Paying down balances, limiting new credit cards and loans and checking your credit report for errors can all work towards raising your score.

- Meet with several lenders. You don’t have to go with the first lender quote you receive. You can shop around to find the best loan to fit your needs—research various mortgage lenders and different loans you might qualify for to put yourself in a stronger position once you are ready to buy a home.

- Crunch the numbers with a mortgage calculator. Once you know which type of loan you qualify for, you can estimate your monthly payments by punching your numbers into various mortgage calculators, such as a 30-year fixed mortgage calculator or mortgage amortization calculator.

- Save money. The more you put down on a home, the less you’ll need to borrow from a lender. This means lower monthly payments and more savings over the life of the loan.

What Affects Current Mortgage Rates?

- Federal Reserve monetary policy. Mortgage rates are indirectly influenced by the Federal Reserve’s monetary policy. When the central bank raises the federal funds target rate, as it did throughout 2022 and 2023, that has a knock-on effect by causing short-term interest rates to go up. In turn, interest rates for home loans tend to increase as lenders pass on the higher borrowing costs to consumers.

- Lenders. A lender with physical locations and a lot of overhead may charge higher interest rates to cover its operating costs and make a profit on its mortgage business. On the other hand, lenders that operate solely online tend to offer lower mortgage rates because they have less fixed costs to cover.

- Your credit. Your individual credit profile also affects the mortgage rate you qualify for. Borrowers with a strong credit history and good score (at least 680) usually receive a lower interest rate, while borrowers with a poor credit score—whom lenders consider high risk—are typically charged a higher interest rate.

Check your rates today with Better Mortgage.

Faster, easier mortgage lending

How To Compare Current Mortgage Rates

Comparison shopping often leads to finding the lowest rates. To get started, you can compare rates and different lender offerings online. Pay attention to the fine print on the websites to see how those rates are determined. For the most accurate quote, you’ll need to apply for a mortgage through various lenders or go through a mortgage broker.

Pro Tip

When applying for a mortgage, you must show that you’re financially stable, so avoid quitting or changing your job—unless it’s for a higher salary—right before or during your application process. Otherwise, lenders may regard your situation as too unstable to afford the monthly payments and deny you a loan. Talk to your lender before making any changes.

Applying for a mortgage on your own is straightforward and most lenders offer online applications, so you don’t have to drive to a physical location. Additionally, applying for multiple mortgages in a short period of time won’t affect your credit score as each application is counted as one query within a 45-day window.

Finally, when you’re comparing rate quotes, be sure to look at the APR, not just the interest rate. The APR reflects the total cost of your loan on an annual basis and any discount points being charged.

Forbes Advisor’s Insight on Current Mortgage Rates and the Housing Market

Predictions indicate that home prices will remain elevated throughout 2024 while new construction continues to lag behind. This will put buyers in tight housing situations for the foreseeable future.

To cut costs, that could mean some buyers would need to move further away from higher-priced cities into more affordable metros. For others, it could mean downsizing, or foregoing amenities or important contingencies like a home inspection. However, be careful about giving up contingencies because it could cost more in the long run if the house has major problems not fixed by the seller upon inspection.

Another important consideration in this market is determining how long you plan to stay in the home. People buying their “forever home” have less to fear if the market reverses as they can ride the wave of ups and downs. But buyers who plan on moving in a few years are in a riskier position if the market plummets. That’s why it’s so important to shop at the outset for a realtor and lender who are experienced housing experts in your market of interest and who you trust to give sound advice.

Frequently Asked Questions (FAQs)

What’s the difference between APR and interest rate?

The interest rate is the cost of borrowing money whereas the APR is the yearly cost of borrowing as well as the lender fees and other expenses associated with getting a mortgage.

The APR is the total cost of your loan, which is the best number to look at when you’re comparing rate quotes. Some lenders might offer a lower interest rate but their fees are higher than other lenders (with higher rates and lower fees), so you’ll want to compare APR, not just the interest rate. In some cases, the fees can be high enough to cancel out the savings of a low rate.

When will mortgage rates go down?

No one knows when mortgage rates will go down. In their September 2023 meeting, members of the U.S. Federal Reserve’s Federal Open Market Committee projected that the federal funds rate—which indirectly affects mortgage rates—might fall from a median rate of 5.6% in 2023 to 5.1% in 2024, 3.9% in 2025 and 2.9% in 2026. But these predictions are based on assumptions that may or may not pan out.

However, the Federal Reserve has indicated it will begin cutting rates in 2024 as the economy cools and inflation continues to fall. Assuming these trends hold steady, you can expect to see lower mortgage rates in 2024.

Why are mortgage rates so high?

Mortgage rates are so high due to a number of economic factors. Supply chain shortages related to the pandemic and Russia’s war on Ukraine caused inflation to shoot up in 2021 and 2022. A resilient economy and robust job market also drive inflation higher and increase demand for mortgages.

When inflation increases, the U.S. Federal Reserve raises its interest rate target for overnight lending between banks, and interest rates throughout the financial sector typically follow suit. From March 2022 to July 2023, the Fed raised its policy rate 11 times, leading to a surge in mortgage rates. A change in demand for 10-year Treasury bonds and mortgage-backed securities also contributed to 2023’s higher rates.

However, the Federal Reserve has indicated it will begin cutting rates in 2024 as the economy cools and inflation continues to fall. Assuming these trends hold steady, you can expect to see lower mortgage rates in 2024.

When should you lock in your mortgage rate?

When you receive a mortgage loan offer, a lender will usually ask if you want to lock in the rate for a period of time or float the rate. If you lock it in, the rate should be preserved as long as your loan closes before the lock expires.

If you don’t lock in right away, a mortgage lender might give you a period of time—such as 30 days—to request a lock, or you might be able to wait until just before closing on the home.

Once you find a rate that is an ideal fit for your budget, it’s best to lock in the rate as soon as possible, especially when mortgage rates are predicted to increase. While it’s not certain whether a rate will go up or down between weeks, it can sometimes take several weeks to months to close your loan.

If you don’t lock in your rate, rising interest rates could force you to make a higher down payment or pay points on your closing agreement in order to lower your interest rate costs.

How long can you lock in a mortgage rate?

Locks are usually in place for at least a month to give the lender enough time to process the loan. If the lender doesn’t process the loan before the rate lock expires, you’ll need to negotiate a lock extension or accept the current market rate at the time.

Even if you have a lock in place, your interest rate could change because of factors related to your application such as:

- A new down payment amount

- The home appraisal came in different from the estimated value in your application

- There was a sudden decrease in your credit score because you are delinquent on payments or took out an unrelated loan after you applied for a mortgage

- There’s income on your application that can’t be verified

Talk with your lender about what timelines they offer to lock in a rate as some will have varying deadlines. An interest rate lock agreement will include: the rate, the type of loan (such as a 30-year, fixed-rate mortgage), the date the lock will expire and any points you might be paying toward the loan. The lender might tell you these terms over the phone, but it’s wise to get it in writing as well.

How do you shop for mortgage rates?

First, start by comparing rates. You can check rates online or call lenders to get their current average rates. You’ll also want to compare lender fees, as some lenders charge more than others to process your loan.

Thousands of mortgage lenders are competing for your business. So to make sure you get the best mortgage rates is to apply with at least three lenders and see which offers you the lowest rate.

Each lender is required to give you a loan estimate. This three-page standardized document will show you the loan’s interest rate and closing costs, along with other key details such as how much the loan will cost you in the first five years.

What are points on a mortgage rate?

Mortgage points represent a percentage of an underlying loan amount—one point equals 1% of the loan amount. Mortgage points are a way for the borrower to lower their interest rate on the mortgage by buying points down when they’re initially offered the mortgage.

For example, by paying upfront 1% of the total interest to be charged over the life of a loan, borrowers can typically unlock mortgage rates that are about 0.25% lower.

It’s important to understand that buying points does not help you build equity in a property—you simply save money on interest.

Forbes Advisor adheres to strict editorial integrity standards. To the best of our knowledge, all content is accurate as of the date posted, though offers contained herein may no longer be available. The opinions expressed are the author’s alone and have not been provided, approved, or otherwise endorsed by our partners.

Was this article helpful?

Thank You for your feedback!

Something went wrong. Please try again later.