Choosing between digital banking vs traditional business banking is one of the most important financial decisions small business owners face in 2026.

The wrong choice can cost you time, money, and operational efficiency. The right one can streamline payments, reduce fees, and help your business scale faster.

This guide breaks down the real differences, costs, and best use cases—so you can make the right decision based on how your business actually operates.

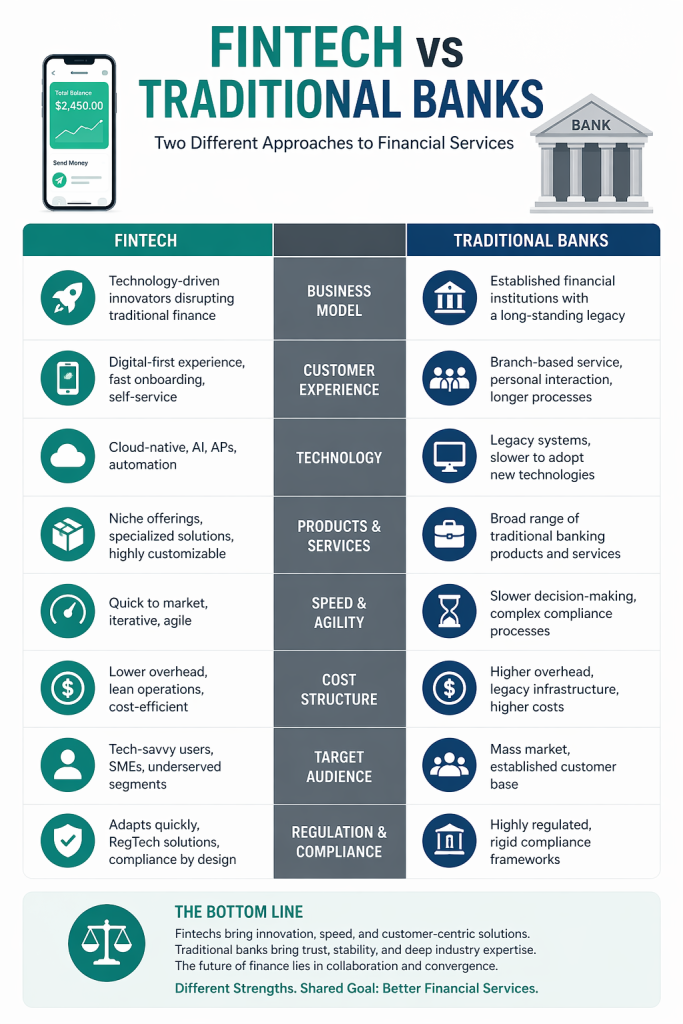

What Is Digital Banking for Businesses?

Digital banking refers to online-first financial platforms that operate without physical branches. These platforms are designed for speed, automation, and lower costs.

Key Features:

- Fully online account setup

- Automated expense tracking

- Integration with accounting tools

- Lower or zero monthly fees

- Fast international transfers

Best For:

- Online businesses

- Freelancers and startups

- Service-based businesses

- E-commerce sellers

What Is Traditional Business Banking?

Traditional banks operate through physical branches and offer a wider range of financial services, including lending, in-person support, and cash handling.

Key Features:

- Physical branch access

- Cash deposit capabilities

- Relationship-based lending

- In-person customer support

- Established trust and security

Best For:

- Cash-heavy businesses

- Retail stores and restaurants

- Established companies seeking loans

- Businesses needing face-to-face support

Key Differences: Digital vs Traditional Business Banking

1. Fees and Costs

Digital banking platforms typically offer:

- No monthly maintenance fees

- Lower transaction costs

- Free or low-cost transfers

Traditional banks often include:

- Monthly account fees

- Wire transfer charges

- Overdraft penalties

Insight: For cost-sensitive startups, digital banking is usually the better option.

2. Speed and Convenience

Digital banking:

- Instant account setup

- 24/7 access from anywhere

- Fast payments and transfers

Traditional banking:

- Slower onboarding

- Limited branch hours

- Manual processes

Insight: If speed matters, digital banking wins.

3. Cash Handling

This is where traditional banks dominate.

Traditional banking:

- Easy cash deposits

- ATM access

- Cash-based operations support

Digital banking:

- Limited or no cash deposit options

Insight: If your business deals with cash daily, traditional banking is essential.

4. Lending and Credit Access

Traditional banks:

- Strong lending options

- Business loans and credit lines

- Relationship-based approvals

Digital banking:

- Limited lending (improving, but still behind)

Insight: For financing and loans, traditional banks are still ahead.

5. Technology and Automation

Digital banking:

- Built-in financial tools

- Real-time analytics

- Integrations with software

Traditional banks:

- Slower tech adoption

- Limited automation

Insight: Digital banking is far more advanced for tech-driven businesses.

Pros and Cons of Digital Banking

Advantages:

- Lower costs

- Faster transactions

- Automation and integrations

- Easy account management

Disadvantages:

- No physical branches

- Limited cash handling

- Fewer lending options

Pros and Cons of Traditional Banking

Advantages:

- Strong lending support

- Cash management

- In-person service

- Established credibility

Disadvantages:

- Higher fees

- Slower processes

- Less flexibility

Which Is Better for Small Businesses?

Choose Digital Banking If You:

- Run an online or service-based business

- Want to minimize costs

- Need automation and speed

- Don’t deal with cash

Choose Traditional Banking If You:

- Handle cash regularly

- Need business loans

- Prefer in-person support

- Operate a physical location

The Smart Strategy: Hybrid Banking

Most successful small businesses in 2026 don’t choose one—they use both.

Example:

- Use digital banking for:

- Daily transactions

- Expense tracking

- Online payments

- Use traditional banking for:

- Cash deposits

- Loans and credit

- Financial relationships

This hybrid approach gives you flexibility, cost savings, and long-term scalability.

Real-World Example

A small e-commerce business uses digital banking to manage payments and automate accounting.

At the same time, the owner maintains a traditional bank account to access credit lines and handle occasional cash transactions.

Result:

- Lower operational costs

- Faster financial management

- Better access to funding

Final Verdict

There is no one-size-fits-all answer.

- Digital banking is ideal for speed, automation, and low costs

- Traditional banking is better for lending, cash handling, and support

For most small businesses, the best choice is a combination of both.

FAQs

Is digital banking safe for businesses?

Yes. Most digital banks use advanced encryption and security systems comparable to traditional banks.

Can I run a business without a traditional bank?

Yes, if your business is fully online and doesn’t handle cash or require loans.

Which option is cheaper?

Digital banking is generally more affordable due to lower fees.

Do traditional banks offer better loans?

Yes. Traditional banks still lead in business lending and credit options.

What is the best option for startups?

Digital banking is usually the best starting point due to low costs and ease of use.

Conclusion

Choosing between digital banking vs traditional business banking depends on how your business operates—not just trends.

If you prioritize speed and efficiency, go digital.

If you need stability and financial support, go traditional.

But if you want to scale smartly in 2026, combining both is the strategy that gives you a real competitive advantage.